Letter to Clients - 2nd Quarter 2024

April 2024

Dear Clients and Friends:

Isn’t it nice when the sun warms up and we can shake off the chill of winter? Like many of you, I am looking forward to more time spent outdoors, even if some of that time will be doing yard work.

At DV Financial, it was a busy tax season. The change from TD Ameritrade to Charles Schwab as our primary account custodian basically doubled the tax documents for every account! Thankfully things should return to normal for 2024.

Coming soon will be the first video mentioned in the last newsletter, although we thought it was going to be released mid-February. Before the end of April, if you are receiving this newsletter via email, you will be receiving a separate email with the first video. It is a 3-minute video introducing DV Financial to your children, grandchildren, or other heirs. May times we do not get to meet your loved ones until we need to, and that is often not the best time to build new relationships. Our hope is that by sending out this video you can forward it to your children. We would like you to encourage them to start building a relationship with us now instead of during a difficult time for everyone.

When you get the video, I welcome your feedback. We have other videos planned to come out periodically throughout the year. With your input, I hope every video is better than the previous one.

Of course, if you are not receiving this newsletter by email, give us a call at 515-255-3354 and we can easily add you to the email list.

A Strong Start for 2024

In August 1864, the Union placed blockades on Confederate ports as part of the Civil War effort. Admiral David Farragut was assigned the task of closing the port at Mobile, Alabama in what became known as the Battle of Mobile Bay. The Union fleet under his command was ordered to proceed into the well defended bay. One of the ships hit a mine and sank, which caused the rest of the fleet to hesitate. Farragut was undeterred and gave the apocryphal order of “Damn the torpedoes! Four bells. Captain Drayton, go ahead! Jouett, full speed!” which became famously paraphrased as “Damn the torpedoes, full speed ahead!”.

A parallel could be made with the current market landscape. Investors are “full speed ahead” navigating a minefield of uncertainties in hopes that the Fed can steer the economy and achieve the elusive “soft landing”. So far this year, it is working.

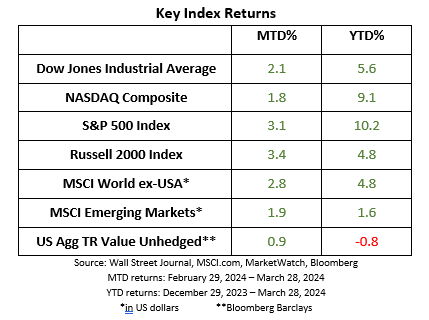

During the opening quarter of 2024, the broad-based S&P 500 Index recorded 22 closing highs, the Dow Jones Industrial Average set 17 new highs, while the NASDAQ Composite posted 4 new highs1.

Last year, a Bank of America analyst dubbed Apple (AAPL), Microsoft (MSFT), Nvidia (NVDA), Tesla (TSLA), Amazon (AMZN), Meta (META formerly known as Facebook), and Alphabet (GOOG/GOOGL formerly known as Google) as the “Magnificent Seven” because those seven companies were responsible for a big chunk of last year’s advance in the S&P 500 index.

A recent article in the Wall Street Journal recently headlined “The Stock Market’s Magnificent Seven Is Now the Fab Four” and pointed out that Apple shares fell 11% in the first quarter, Tesla dropped almost 30%, while Alphabet sputtered much of the quarter but rallied at the end to finish up almost 8%. But it is not just the Fab Four which performed well. All sectors of the S&P 500, except real estate, posted gains in the first quarter. The repeated new highs of the major market indexes also suggest the rally has broadened.

The market was encouraged that as the quarter ended inflation had subsided, and the Federal Reserve is considering up to three quarter-point rate cuts this year. LSEG, formerly Refinitiv, reports that the economy is expanding, and that corporate profit growth has been strong.

It has been a good time to be a long-term investor who adheres to a diversified 2and disciplined strategy, but market corrections are inevitable. The next pullback is just one unexpected headline away.

When stock prices tumble, it can be tempting to move away from equities and embrace cash. However, such strategies have rarely proven to be profitable due to the extreme difficulty in deciding when to make the moves out and then later back into the market. This is why we do not advocate changing your investment strategy based on market action(s). Instead, we rely on the proven long-term track record of diversified investing based on your needs and tolerance for risk.

Understanding Social Security Retirement Income

The social security retirement income benefit was designed to provide a basic income to supplement retirement resources. It was never intended to fully cover the cost of living in retirement. The benefit each retiree receives is based on several factors including the Average Indexed Monthly Earnings (AIME) and your age when you begin drawing benefits.

AIME is based on a person’s highest-earning 35 years of work, adjusted for inflation, and averaged to produce a monthly figure. AIME is used to calculate the Primary Insurance Amount (PIA) which determines the Social Security Retirement Income Benefit. Higher AIME values lead to higher benefits.

To improve your AIME, you can work more years or increase your income. Suppose you started working at age 30 and worked continuously to age 65. You would have exactly 35 years of income. If you continue to work, you could replace your lowest income year used in the AIME calculation, provided your current income was greater than your lowest income.

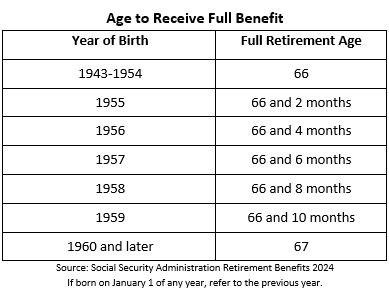

The earliest you may start Social Security retirement benefits is when you reach age 62. Until you reach “Full Retirement Age”, if you continue to work there is a limit to how much you can earn without having your benefit reduced. Your “Full Retirement Age” is determined by the year you were born.

For example, if you were born in 1956 your Full Retirement Age is 66 and 4 months. If you were born in 1960 or later, the Full Retirement Age is 67. While you may receive social security benefits before your Full Retirement Age, your benefits will be permanently reduced. Conversely, the longer you wait to begin benefits, the larger your monthly benefits will be. Once you reach Full Retirement Age, your benefit increases by 8% per year until you reach age 70 at which time you maximize the percentage of your PIA payable.

You could describe strategies regarding when to begin drawing Social Security retirement benefits as trading more payments of a smaller amount for fewer payments of a larger amount. The best strategy is largely determined by how long you live. Generally, the break-even point of starting benefits later is in the late 70’s. If you continue receiving larger benefits into your 80’s, it is likely that you will get more money from Social Security than if you started earlier. If you do not live into your late 70’s you would have received more money if you had started earlier.

Each spouse of the marriage is entitled to their own social security benefit based on their own AIME, although a non-working spouse may apply for a spousal benefit which is up to half of the working spouse’s benefit. At the death of the first spouse, the surviving spouse may keep the higher of their own benefit or the deceased spouse’s benefit.

One strategy for Social Security income is to begin the spouse with the lower PIA as early as practical without incurring a reduction if they continue to work, while the spouse with the higher PIA maximizes their benefit by delaying until age 70. As long as either spouse survives into their 80’s or longer, this may maximize the total Social Security income the couple receives.

Planning for Social Security can feel like entering a maze. The options can be overwhelming, and it is easy to get disoriented. While I have tried to provide a high-level overview, it is impossible to cover every nuance of a program as complex as Social Security. Your individual situation is unique, but too many people do not begin to consider Social Security strategies until they are ready to apply for benefits.

Get Comfortable

Most people only deal with retirement issues, such as Social Security, once in their lifetime which means they are making very important decisions without the benefit of experience. What a terrifying proposition!

At DV Financial, we have over 35 years of experience helping people make all kinds of retirement decisions, including Social Security strategies. Our mission is to help you get comfortable with those decisions by leveraging on our experience. If you (or anyone you know) wants to discuss Social Security, or any other financial issues, we are here to help. Just give us a call.

Sincerely,

Art Dinkin, CFP®

1 Dow Jones Newswires

2 Diversification does not guarantee a profit or protect against a loss in a declining market. It is a method used to help manage investment risk.

This newsletter contains general information that may not be suitable for everyone. The information contained herein should not be construed as personalized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security.

Not associated with or endorsed by the Social Security Administration or any other government agency.

Indices are unmanaged and investors cannot invest directly in an index. Unless otherwise noted, performance of indices does not account for any fees, commissions or other expenses that would be incurred. Returns do not include reinvested dividends.

The Dow Jones Industrial Average (DJIA) is a price-weighted average of 30 actively traded “blue chip” stocks, primarily industrials, but includes financials and other service-oriented companies. The components, which change from time to time, represent between 15% and 20% of the market value of NYSE stocks.

The Nasdaq Composite Index is a market-capitalization weighted index of more than 3,000 common equities listed on the Nasdaq stock exchange. The types of securities in the index include American depositary receipts, common stocks, real estate investment trusts (REITs) and tracking stocks. The index includes all Nasdaq listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds (ETFs) or debentures.

The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. It is a market value weighted index with each stock's weight in the index proportionate to its market value.

The Russell 2000 Index is an unmanaged index that measures the performance of the small-cap segment of the U.S. equity universe.

The MSCI All Country World Index ex USA Investable Market Index (IMI) captures large, mid and small cap representation across 22 of 23 Developed Markets (DM) countries (excluding the United States) and 23 Emerging Markets (EM) countries*. With 6,062 constituents, the index covers approximately 99% of the global equity opportunity set outside the US.

The MSCI Emerging Markets Index is a float-adjusted market capitalization index that consists of indices in 21 emerging economies: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey.

Barclays Aggregate Bond Index includes U.S. government, corporate, and mortgage-backed securities with maturities of at least one year.